Dec 28, 2020 ●10 min read

How Is Fintech Different from Banks?

The banking industry has undergone a transformation with the introduction of technology. With the introduction of mobile banking, smart chip technology in ATMs, online transactions, and much more, there is no looking back. With the world moving to provide customer satisfaction and ease of services in every industry, the financial sector too saw a shift with emerging and ever-evolving Fintech firms.

There have been many arguments on whether Fintech can eliminate banks from the industry or is it just a hype that has been created by some new entrants in the industry. In this article, we will talk about many such questions and look at the differences between banks and fintech firms and how they contribute to the financial sectors in their own individual ways.

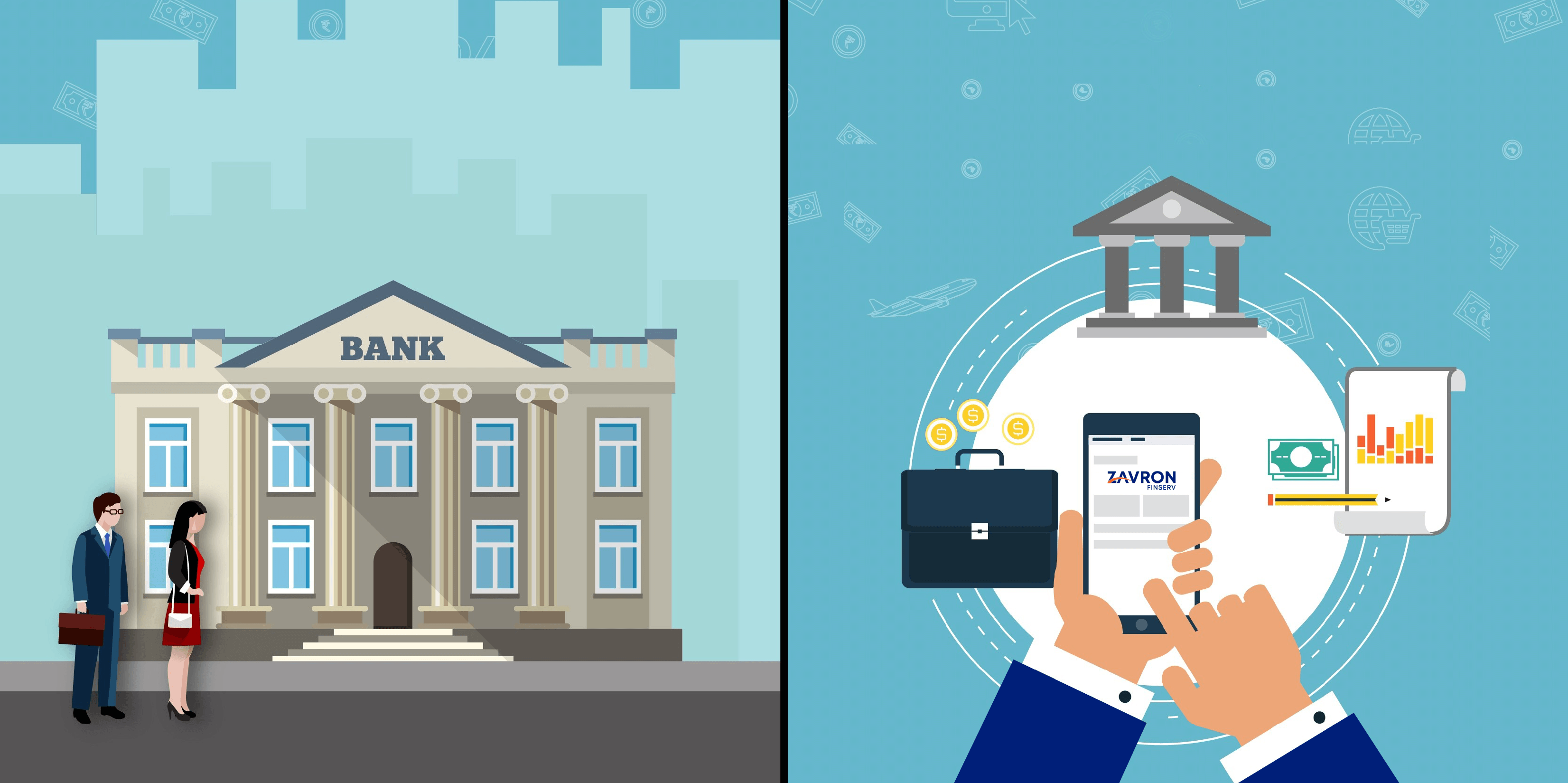

Bank vs Fintech

Before diving right into the matter here, let us understand what are these two entities. The most common and obvious definition of a bank states that it is a financial institution that receives deposits and gives out loans. Whereas, fintech, i.e. ‘Financial Technology’ can now be understood as financial services for consumers that are prompted by the use of technology in the form of mobile banking, online banking, and alternative financing.

Difference between Fintech and Banks

Banking has evolved significantly over the past few years. With the advent of technology into the picture, customer experience took a primary stage in the overall process. Hence, the major difference between a fintech firm and a banking institution starts from consumer satisfaction. Here are a few major differences that you can take into consideration while pointing out the difference between banks and fintech firms.

Consumer-centric services

One of the major differentiators between Fintech firms and Banks is their approach towards the customers. While banks are known to work around financial risks and securities, fintech startups across the globe have made consumers their primary focus.

Providing financial services and creating a seamless, hassle-free experience for the customer is the major focus of fintech firms. The customer relationship created by fintech is more personalized, open, and transparent. Customers can get their problems resolved at any given point with a 24/7 customer service option. Whereas, banks have functioned in the traditional ways thereby missing out on an opportunity to deliver excellent customer experience and move to new and improved ways of banking.

Digitization

Although banks across the globe have adopted technology and function around digitization, however, due to rigid organizational structures and heavy reliance on physical processes banks are yet to fill huge gaps. Fintech however heavily relies on technology. Looking at the market demand for quick and safe services, fintech adapted to automation, IoT, AI/ML to accelerate processes and keep the consumer data safe. Resultantly, fintech offers products and services such as e-wallets, mobile banking, online transactions, biometric censors for security, etc. that are secure and provide quality with less or no scope of mistakes.

Target Segment

Many can argue that banks cater to all the target segments from all the tier groups, however, there are major gaps that remain unfulfilled hence making it a hassle for people from lower-income groups to access traditional banking services. But fintech firms these days ensure that they keep a tab on these gaps and reach to customers from across all the segments irrespective of age or geography with the best products and offers, especially when it comes to providing lending services to the untapped and unserved consumer segment of rural and urban areas. Fintech has higher potential coverage since 80% of the Indian population has shifted to mobile banking. Hence, Fintech can cater to their needs better than the 35% of banking services available currently to the consumers in terms of mobile banking.

Organizational Structure

The organizational structure of the banks and fintech have some major differences. The legacy infrastructure of banks and traditional functionalities restrict quick services and hinders the introduction of technology for new and better products to address consumer concerns. Hence, they easily drain out of innovation and productivity. The process-oriented and stringent regulatory frameworks often create a roadblock. Fintechs comparatively work under a simplified regulatory framework. Since they are focused on a customer-first approach, their operating model is flat which promotes innovation and technological advancements with a huge data bank they acquire from the customers. Fintech often introduces niche products by analyzing data and market requirements on the root level.

Final Words

The new players in the market are booming. Fintech firms have grown exponentially and the market predictions work in their favor too, however, banks are quickly adapting to new ways and technology. And it is safe to say that the collaboration between banks and fintech will only lead to faster growth, innovation, profits, and better customer experience.

Beyond viewing Fintech firms as competitors, banks are embracing it as an opportunity to streamline processes, increase revenue, and generate new business. Not only can they improve the health of traditional institutions, but fintech can be used as a powerful tool to retain customers and know their preferences. Apart from customer experience, banks are also looking at solving industry pain-points like securing credit card processing, loan processes, and money transfer.

FAQs

Can Fintech replace banks?

Ans. It would be unfair to say that banks can be replaced by Fintech. However, banks are evolving and quickly adapting to innovation and technological advancements to improve business, economics, and consumer experience as well.

Why do banks need Fintech?

Ans. To keep up with the ever-evolving demands of the market and cater better to the consumer needs of a quick and seamless banking experience, banks have started including Fintech into their system.

Why is Fintech important?

Ans. Bank transfers, transactions, bill payments, loan applications, and many other banking services are carried out using technology seamlessly; hence the inclusion of Fintech is important.

What is the impact of Fintech?

Ans. Fintech has had a major impact on the overall financial sector. It has helped banks and consumers across the globe to move from the traditional banking system to technologically advanced products and services.

Is Fintech safe?

Ans. Due to heavy reliance on technology, there are chances of a potential data breach, however, Fintech firms ensure safety at multiple levels since they adopt end-to-end solutions to analyze frauds and secure customer data.

What should banks do to incorporate Fintech in their regular framework?

Ans. The foremost requirement is that the institution should be motivated from the top to introduce technology and innovation. Further, a proper fintech strategy in place to connect new ideas and business needs by analyzing the pros and cons of the proposed strategy.

LICENSED BY RBI

ZAVRON FINANCE PVT LTD

RBI License no.:- N-13.02268

CIN:- U67100MH2017PTC292183