Jan 22, 2021 ●15 min read

How to Improve Credit Score After Default?

We have seen the world fret over credit scores and credit reports. Loan defaulters, low credit scorers face great levels of difficulties when it comes to applying for a loan with banks. They are subjected to rejections. But wait, what is a cibil score anyway and why is it so important? Before getting into how you can improve your credit score, we want to throw some light on what is a credit score and what is a good credit score.

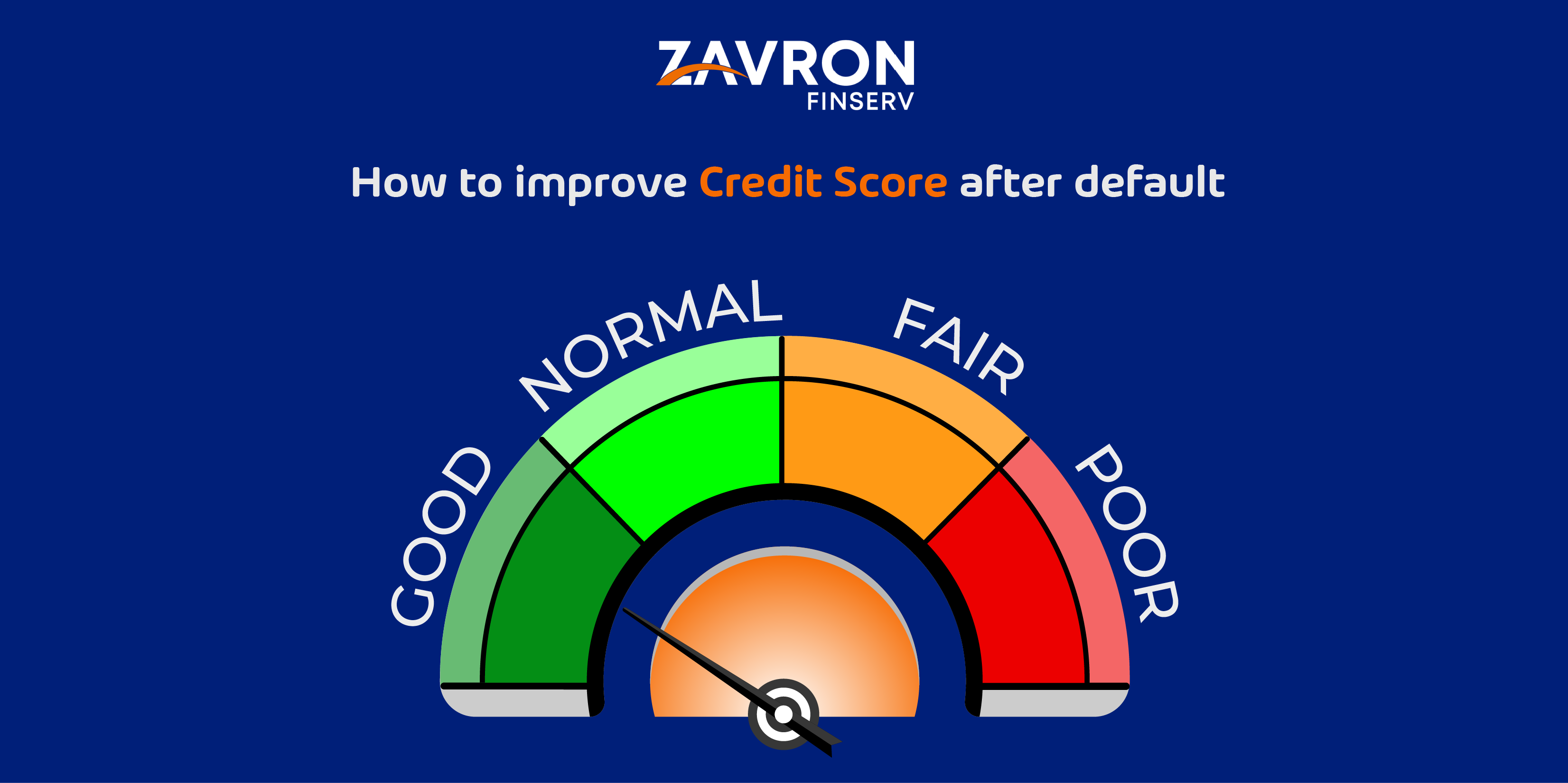

A credit score is basically a number between 300-850 that determines an individual’s creditworthiness. The 3 digit numbers are potential indicators to lenders to determine whether they should engage in underwriting loans to the borrowers. Therefore, the higher the score, the better the chances of loan approval. A good credit score above 700 is considered to be good; here is a breakdown of the cibil score and how it is viewed in the loan market;

● 300-579: Very Poor

● 580-699: Fair

● 670- 739: Good

● 740-799: Very Good

● 800-850: Excellent

Now that you have a fair idea of the CIBIL score, we would want to highlight how you can improve it if you have been on the defaulters’ list. In this article, you will find the answer to the question, if it is possible to improve credit score after default? If yes, then how? We have enlisted a few points that will help you in improving your score and better your chances of getting a loan in the future without any rejections or complications.

Is it possible to improve your Credit Score after Default?

If you are worried that your low credit score after default cannot be improved, you should stop right there. You can surely improve your credit score with a few measures and careful financial stand. However, it is advisable to repay your loan in time to avoid unpleasant surprises such as loan application rejection since it indicates your inability to pay back personal loans and financial stress.

Ways to Improve Credit Score after Default

There are several ways to improve your credit score after default. But as mentioned earlier, the borrowers must ensure that their loans and debts are paid well in time to avoid being in a defaulters list and avoid any rejections in the future when in financial needs. Here are a few tips to improve credit score after default.

Clear old debts and loans

Yes, the foremost step is to clear off all the loans and debts. Make payments and make sure that they are done in time in the future. Since untimely payments are the biggest contributors to the default, you can set reminders to avoid missing the last dates or any delay in paying EMIs.

Do not exhaust your credit limit

Credit limits if fully-utilized can pose a problem when you are trying to improve your credit score. Your credit utilization ratio has a huge impact hence you can customize your credit limit or restrict your usage of the credits available. If you exhaust the limit, it will negatively impact the credit score, hence decreasing the chances of improving it. Based on your expenses, plan and coordinate with your lender to customize the limit for you.

Maintain your accounts

When you are trying to rebuild a good credit score, make sure that your credit and debit accounts are well maintained. Your older accounts will be helpful in recovering from the jolt a little faster and furthers your chances of availing of instant personal loan in the future with approval. Remove any defaults associated with your accounts and let the negative report drop off the accounts.

Keep a check on your CIBIL

If you are certain that your payments have been on time always and you are doing everything right when it comes to managing your debts and finances then consider looking at your CIBIL report. It can happen at times that the CIBIL report may record irregularities by mistake. Spot them and get them rectified to ensure your credit score is unaffected and strong.

Maintain a balance

Did you know your secured and unsecured loans can have an impact on the credit score? Well, yes. If you have not been maintaining a balance between your secured and unsecured loans, it can have a negative impact. Try to strike a proportionate ratio between the two to not impact your CIBIL Report negatively.

Take a loan with longer repayment options

If you are borrowing from banks or other lender companies, ensure that the repayment tenure is a little longer. This will give you enough time to arrange for funds and lower your EMIs. Eventually, you will end up paying on time and avoid any delays whatsoever, thus improving your credit score substantially.

Don’t send multiple loan queries

Even though you might have cleared off all the debts and loans, you still have to show a good record. If you are sending multiple loan queries from your accounts, your credit score will be impacted negatively. It will throw you in bad light hence lowering your credit score.

FAQs

How long does it take to improve credit score?

Ans. Usually, the default stays upto 6 years in the file regardless of you repaying the debt. But once it is out of the files, you can see an improvement in your credit score.

Can you get the default removed from the credit report?

Ans. If your credit report is mistakenly marked as default, your lender can remove it. You will have to put in the request to get the necessary changes in implementation.

How can you quickly fix your credit score?

Ans. Although there is no quick fix, some immediate actions may be helpful. Just pay your debts in time, and maintain your accounts, check for any mistakes in the credit report and be consistent in repayment of outstanding payments.

How bad is having a zero balance on a credit card?

Ans. Full-utilization has a negative impact on the credit score. It is not advisable to overuse your credit card limits.

Is it good to pay off credit card debt in full?

Ans. Credit card debt if paid fully in a month is excellent to maintain a good credit history and increases your credit utilization history.

Quick Links: Personal Loan | Urgent Business Loan | Used Car Loan | Two Wheeler Loan

LICENSED BY RBI

ZAVRON FINANCE PVT LTD

RBI License no.:- N-13.02268

CIN:- U67100MH2017PTC292183